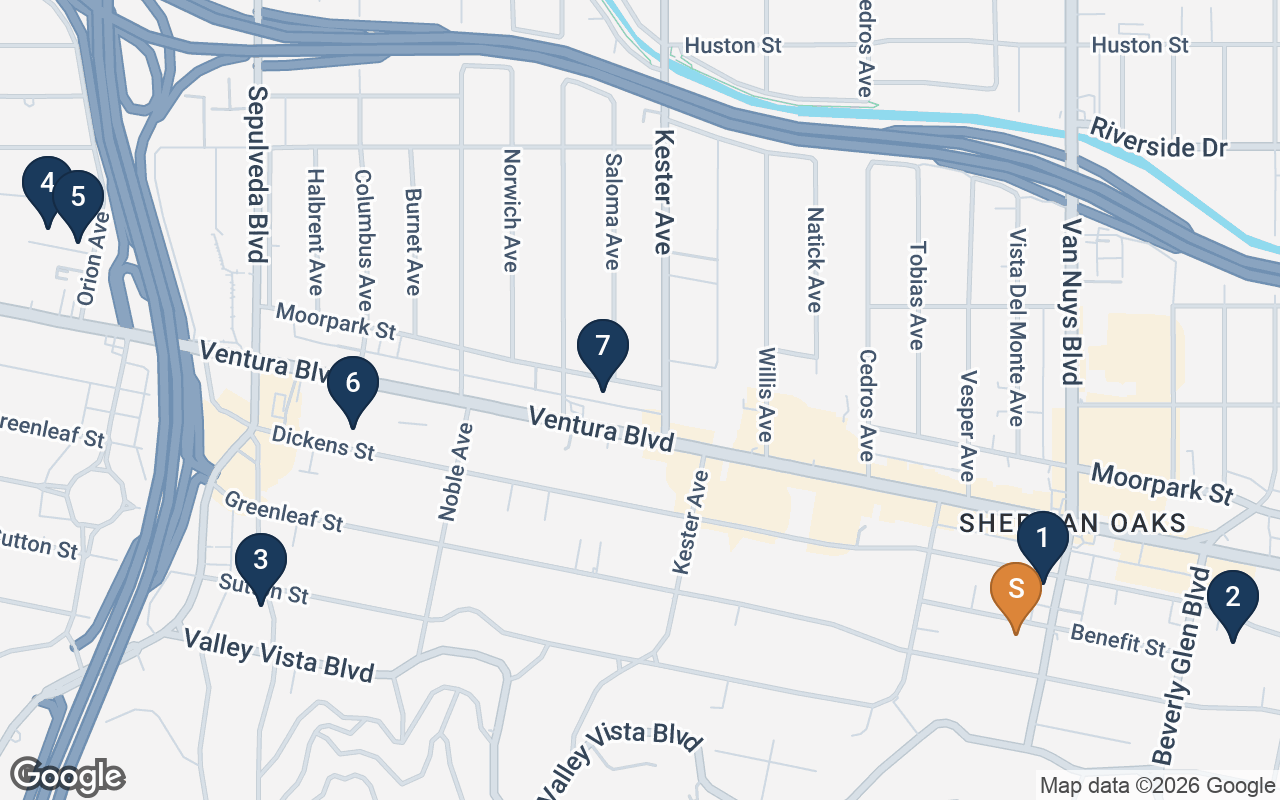

1. 4323-4329 Van Nuys Blvd - A two-parcel, ten-unit portfolio that closed in March 2026 literally around the corner from the subject (0.1 mi), purchased by Crestview Elementary LLC at $400,000/unit - the strongest per-unit print in the recent RSO set and the clearest evidence of what buyers pay for this exact pocket.

2. 14318 Dickens St - A six-unit 1948 walk-up three blocks east, closed November 2025 at $266,667/unit. The nearest similar-size sale to the subject; a conventional occupied-RSO print without the subject's vacancy or expansion story.

3. 4321 Saugus Ave - A twelve-unit 1953 building closed August 2025 at $3,110,000. Larger asset, institutional-adjacent buyer pool; anchors the mid-range $/SF for the submarket.

4-5. 15461 & 15445 Moorpark St - Adjacent 1957 sister buildings (11 and 8 units) that closed the same day in April 2025 for $2,450,000 and $1,700,000 respectively - classic occupied legacy-tenancy pricing at $212,000-$223,000/unit, the deep-discount end of the RSO band the subject's vacancy avoids.

6. 15207 Dickens St - Nine units, 1955, closed April 2025 at $233,333/unit. Another fully occupied print confirming where tenanted RSO product trades.

7. 14938 Moorpark St - Seven units, 1960, closed January 2025 at $359/SF - the highest $/SF in the sold set, driven by smaller total area, and a bridge toward the $/SF the active listings now ask.